One search carried out to prepare a new strategic study of the Greener – which will be launched soon – points out that the photovoltaic market in centralized generation remains heated in Brazil and with greater focus on ACL (Free Contracting Environment).

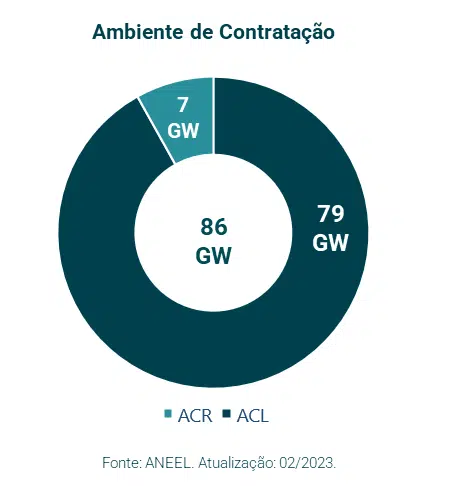

According to the research and consultancy company, around 91% with 86 GW of power in projects awarded until February this year were destined for the Free Energy Market, as shown in the image below.

“A large part of this movement comes from a gradual process of market opening, which receives an increasing number of consumers due to the decrease in demand limits for migration”, highlights Greener.

Of the total of 86 GW until February, around 73.6 GW (85.6%) were related to photovoltaic projects with construction not started, while 4.9 GW (5.7%) in projects with construction started and another 7.5 GW (8.7%) in plants with commercial operation.

Among Brazilian states, Minas Gerais is that it has the largest amount of power coming from large solar projects, with 39% of the 86 GW granted. Next, Piauí (13%) and Bahia (12%) appear in the study.

Despite the large volume of projects awarded in the country, the study of Greener warns of some points of attention in the development of these plants, such as the challenges related to connection – conditioned on the availability of drainage margin.

“With a significant increase in the number of projects granted, Minas Gerais, for example, suffers from denials of access or operational restrictions that can impact the viability of projects. In turn, drafting energy purchase and sale contracts in a scenario of low prices in the short-term market and high interest rates is a challenge for entrepreneurs who wish to invest in this market”, highlights the study.

In this way, Greener finally points out that questions such as “What alternatives to gain project efficiency?”; “How to enable attractive solar PPAs?” or “How should market opening influence business models?” continue to be important points of reflection for investors in the sector.