While the market fights over pennies on the dashboard, the integrators who will lead in the coming years have already discovered where the real game is decided.

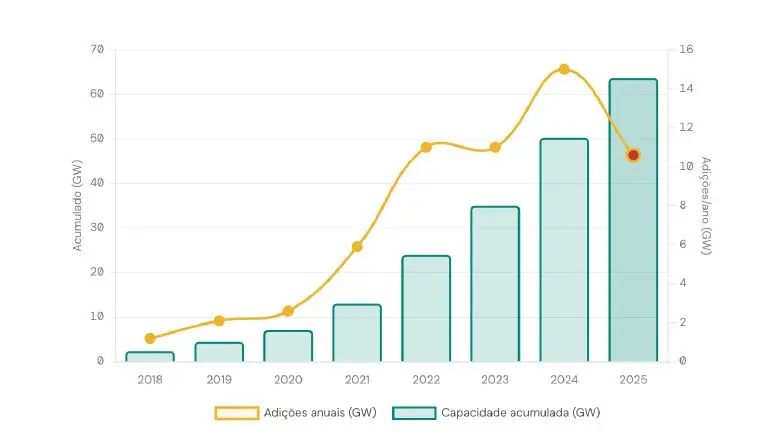

Brazil ended 2025 with 63,7 GW of installed solar capacity (the second largest source in our electricity matrix), representing 24,5% of the total generated. We are the 4th largest solar market in the world. And, paradoxically, 2025 was the first year of significant contraction in the sector's recent history: a 29% drop in new installations, with 2026 projected to be the worst. second consecutive year of decline.

The market has stopped growing easily. For the integrator who doesn't want to compete solely on price, what remains is precisely the asset that has always been there, underutilized: the post-sales relationship.

A market that grew too fast for its own good.

In 2012, Brazil had 7 MW of installed photovoltaic solar energy. Thirteen years later, by the end of 2025, that number had reached 63,7 GW, with 43,7 GW from distributed generation and 20 GW from large-scale plants. This represents a growth of more than 9.000 times in just over a decade. Solar energy has become the second largest source in the Brazilian electricity matrix, responsible for 24,5% of the country's operational installed capacity, according to [source needed]. ABSOLAR.

But the most important data for the integrator is not that. It's what happened in 2025: for the first time in years, the market for new installations shrank, and shrank sharply. Only 10,6 GW were added that year, a 29% decrease compared to the 15 GW of 2024.

Investments fell even further: from R$ 54,9 billion in 2024 to R$ 32,9 billion in 2025, a drop of 40%. And the projections of ABSOLAR Projections for 2026 indicated that it would be the second consecutive year of decline. Easy growth is over. The era of efficiency, reputation, and relationships has begun.

The number of active integrators in Brazil has jumped to tens of thousands over the last decade. The result: price competition in every proposal, squeezed margins on every project, and a client who has learned to compare prices using Google before even answering the first phone call from the salesperson. In this scenario, fighting over price is not a strategy, it's a race to the bottom.

Market context 2025

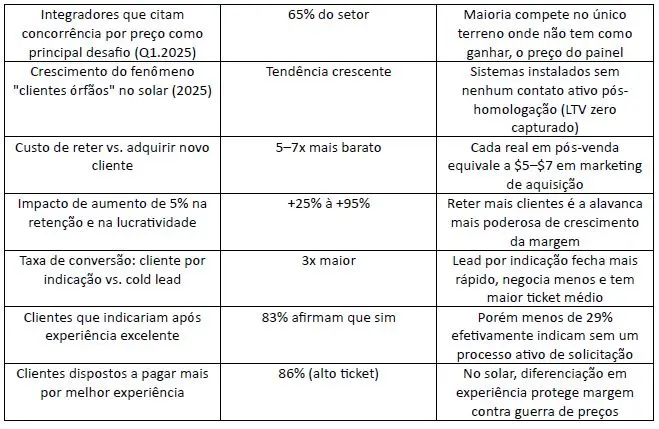

A Greener survey of 1.188 integrators regarding the first half of 2025 revealed: 65% cite price competition as the biggest obstacle.A 46% drop in the monthly volume of quotes compared to the same period in 2024; and the growth of the phenomenon of "orphan clients" (consumers without active support from the company that installed the system). In the first two items, the market imposes the problem. In the third, the integrator creates the problem itself, and the solution is entirely in its hands.

The commoditization trap and the antidote that most people ignore.

In commoditized markets, there are two possible survival strategies: being the cheapest (cost leadership) or being the most valued (differentiation). Cost leadership in solar energy is, in practice, unfeasible for the vast majority of small and medium-sized integrators; they lack the scale to compete with distributors or large networks. Therefore, differentiation remains the only remaining option.

And here's the paradox that became more acute in 2025: the market contraction didn't come alone. It was accompanied by a rise in the price of kits; industry experts estimate that the increase has been up to... 35% reduction in the cost of solar kits by 2026 Regarding the end of 2025, this reflects the withdrawal of Chinese tax incentives on exports and the increased cost of silver as a raw material.

Less new demand, more expensive equipment, more aggressive price competition. It is precisely in this scenario that the installed customer base becomes the integrator's most strategic asset, and after-sales service, the only lever that does not become more expensive with the dollar.

The main source of differentiation in the solar market isn't the product, it's the service. Tier 1 panels from the same manufacturer are sold by dozens of different integrators. What can't be easily copied is the customer experience with you. after the system becomes operational.

“The panel is a commodity. The installation is a commodity. What cannot be copied is the experience of being cared for after the proposal is signed.”

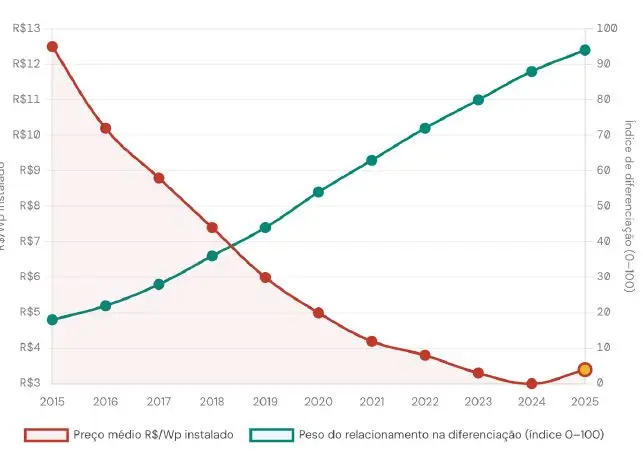

The graph below illustrates the phenomenon with real data: while the average price per installed watt has fallen by more than 60% in the last ten years in Brazil (reflecting the global drop in module prices), the perception of value based on relationships and reputation has become the only sustainable vector for differentiation.

The reading is clear: as prices collapse and the market for new installations contracts, the weight of relationships in repurchase, expansion, and referral decisions grows proportionally. The integrator that built a solid after-sales reputation throughout the growth cycle will, in 2026, be reaping the rewards of an asset that its cheaper competitors simply do not have.

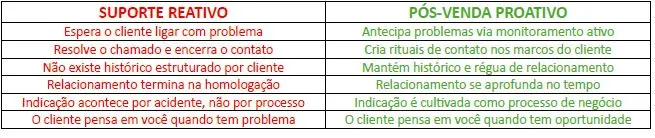

Support is not after-sales service, and confusing the two is proving costly.

This is where most integrators get stuck. When I ask, "Do you have after-sales service?", the answer is almost always: "Yes, we assist the customer when there's a problem." That's not after-sales service. That's reactive support. The difference between the two is structural and financially significant.

The consequence of this confusion is measured in money. A client who only reminds you when the inverter fails is a client who will receive a competitor's offer when the neighbor asks about solar. A client who receives your quarterly report, who remembers the savings generated on the system's anniversary, who was proactively notified when generation dropped—this client doesn't need you to reinforce your value proposition. They've already experienced it.

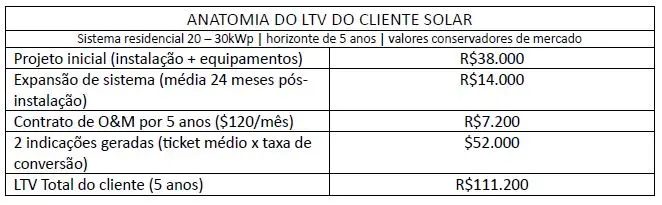

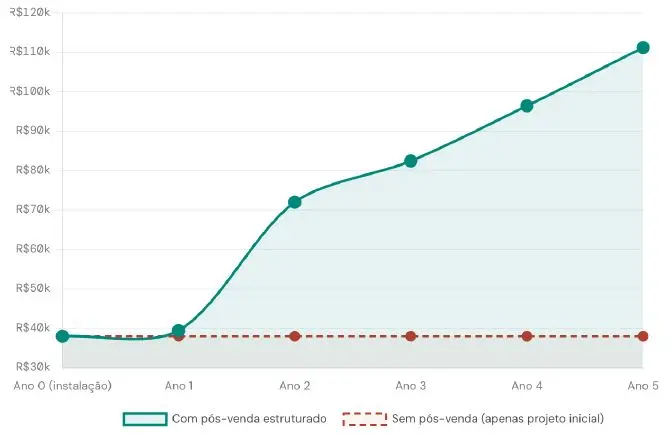

The true value of a solar customer: the LTV that nobody is calculating.

Here's the article's most powerful argument. Most integrators assess a client's value based on the project's ticket price—and that's a brutal financial analysis error.

The true value of a well-cared-for solar customer is the sum of multiple revenue streams over time: the initial sale, system expansion, referrals generated, and operation and maintenance (O&M) contracts.

Let's look at an exercise using conservative market figures for a mid-sized residential system:

A single customer who generated just 2 referrals (an absolutely achievable number for those who do post-sales work well) represents over R$110 in potential revenue. Compare that to the amount your marketing team invests to acquire a new customer through paid media. The equation changes completely.

The problem is that this LTV (Lifetime Value) is only achieved if the relationship is cultivated. Without structured after-sales service, the client expands the system with the competitor who came first, doesn't generate active referrals, and the O&M (Operations and Maintenance) contract (if it exists) becomes a burden that no one actively follows up on.

Reference data

The market benchmark for a healthy LTV/CAC ratio is no. minimum 3:1In other words, each customer should generate at least three times the acquisition cost. In a solar company with a well-structured after-sales service, this ratio... It can easily reach 8:1. Or more, completely transforming the integrator's growth equation.

What the market says about retention and relationship building.

Global data on customer management in high-ticket services is consistent and alarming for those who have not yet structured their after-sales service.

The Greener study, conducted with 1.188 integrators for Q1 2025, identified the growth of the "orphan customer" phenomenon (installed systems whose owners no longer have active contact with the integrator) as one of the main trends in the sector. This reflects the lack of after-sales service becoming a market reality.

These figures aren't specifically from the solar sector—they're the result of decades of research in customer management and customer experience in high-value services. Solar perfectly fits this profile: high-ticket product, long lifecycle, customer with strong emotional motivation, and high referral potential. And in 2025–2026, with the new installation market contracting, the relevance of this data has never been more direct for the Brazilian integrator.

The data that changes everything in 2026

A ABSOLAR It was confirmed in January 2026: the solar market contracted by 29% in 2025 and projects a further contraction in 2026. In a scenario of fewer new projects, the integrators that survive and grow are those that dominate the installed base.

A study by Bain & Company shows that increasing customer retention by just 5 percentage points raises profits by 25% to 95%. For an integrator with 200 active clients and average revenue of R$30 per project, this could represent dozens of "extra" projects per year without spending a penny on acquisition marketing. By 2026, this is no longer an optional strategy. It's a survival strategy.

Where to begin: the minimum viable post-sales framework

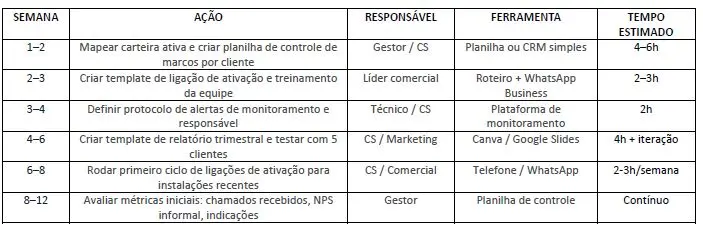

Structuring post-sales service doesn't require an entire department or expensive software. It requires process, consistency, and intention. The following framework can be implemented in any integrator in less than 30 days, using the resources you already have.

(01) First 30 days

Activation link and educational onboarding

Between 7 and 15 days after activation, call the client. Objective: to confirm that they understand how to read the monitoring app, calibrate generation expectations for the period (especially if it's winter), and open a channel of trust. This call alone reduces calls by more than 60% in the first 3 months.

(02) Month 1 – First impact

Proactive contact before the first post-solar bill.

The first electricity bill after the system is installed is a moment of great anxiety for the customer. If the generation didn't meet the promise (due to seasonality, shading, or calibration), they will be disappointed. Call before the bill arrives, provide context for the number, and demonstrate that you are monitoring the situation. This transforms a potential source of dissatisfaction into a moment of trust.

(03) Quarterly

Customized performance report

Every three months, send a simple report with: accumulated generation during the period, estimated savings in reais, CO₂ avoided (a highly emotionally impactful statistic), and a comparison with the project forecast. It doesn't need to be an elaborate document; a WhatsApp message with a screenshot of the app and a paragraph of your own will suffice. What matters is consistency.

(04) Annual – High conversion

System anniversary ritual

On the 1-year anniversary, send or deliver a complete performance report (real savings generated), projections for the coming years, and environmental impact data. This is the ideal time for two conversations:

(a) system expansion or new products, and

(b) referral request. Customer at peak satisfaction, with real return data in hand, converts a lot.

(05) Continuous · Monitoring

Proactive alert protocol

Define a simple protocol: any system offline for more than 24 hours, with a generation drop exceeding 15% without a weather-related justification, or with a datalogger communication failure, will receive a notification from you before the client even notices. This practice transforms passive monitoring into an active differentiator and generates spontaneous mentions: "my integrator notified me before I even realized it."

The time investment in this framework is less than 10 hours in the first two weeks and less than 3 hours per week after the implementation phase. For a portfolio of 100 active clients, the expected return in reduced calls, increased referrals, and initial O&M contracts justifies the effort in less than 90 days.

Conclusion

After-sales service is not a cost area. It's the integrator's area of greatest return, and in 2026, with the market contracting for the second consecutive year, it has become the most strategic area of the business. In a scenario of fewer new projects, more expensive kits, and fierce price competition, the relationship with the installed base is the only asset that doesn't increase in value with the dollar, doesn't depend on credit, and cannot be copied by the competitor who showed up at your client's door with a panel 5% cheaper. The integrator who understands this now (and acts on it) will not only survive the consolidation that is underway. They will be the ones who lead it.

Sources and references:

1. ABSOLARSolar Photovoltaic Infographic, Jan. 2026 (via Exame); installed capacity, contraction in 2025 and investments.

2. ABSOLARProjections for 2026 (via Portal Solar / pv magazine Brazil, Dec. 2025); estimated 10,6 GW and R$ 31,8 billion.

3. Greener. Strategic Study of GD — H1 2025 (1.188 integrators); challenges, orphaned clients, budget cuts.

4. Canal Solar. "High prices for solar panels," April 2026; projected 35% increase in solar kit prices in 2026.

5. Portal Solar / CCEE / ONS; evolution of average price per Wp installed in Brazil 2015–2025.

6. Bain & Company. “The Value of Customer Retention”; the impact of retention on profitability.

7. Frederick Reichheld / HBR — “Prescription for Cutting Costs”; retention cost vs. acquisition cost.

8. Jan Carlzon. “Moments of Truth”; a framework of customer touchpoints.

9. PV magazine Brazil, Apr. 2025; solar reaches 55 GW, 22% of installed capacity, M&A +25% in Q1 2025.

The opinions and information expressed are the sole responsibility of the author and do not necessarily represent the official position of the author. Canal Solar.

An answer

Indeed, how the customer is treated after the sale makes all the difference; it's more important than the purchase process and the delivery itself. A customer who feels supported and "seen" by the company will recommend it to other customers. This sets companies apart in the sector.